You have found the perfect home, made an offer, and accepted by the seller. You have ordered a home inspection, and any issues have also been resolved. You are now ready to close the mortgage loan financing your home purchase.

It is normal to feel anxious during closing – especially as the day nears – because you will sign the documents that transfer the ownership of the house to you. Additionally, you will have to pay closing costs and all applicable taxes.

This can make it seem a little stressful. You can reduce stress by knowing exactly what you will need to bring to closing. This will eliminate any unexpected surprises during the final leg of your home-buying adventure.

For more information about the process, please review the steps below. This will show you what your lender and you will need to do before closing.

What is the average time it takes to close?

It takes on average 30 to 45 days to close a home. This includes filling out the mortgage loan application and showing up at closing. The closing day is the day that you sign all your paperwork. It takes about one to two hours, depending on how everything goes.

The time it takes to close a deal on a house depends on how organized you are, the experience of your loan officer, and the reliability of its seller.

Understanding your documents

It is important to take inventory of all your closing documents so that you and your lender are prepared for closing. This will make it easier for you to find and send any requested forms at the last moment, which can help speed up the closing process.

A list of documents that you require and deadlines to submit them can be created. You can check them as you send them to the lender. Also, mark the date that they were sent. To confirm they were received, you will need verification.

Closing disclosure

Your lender must send you the Closing Disclosure no later than three business days before closing. This document contains all the pertinent information about your loan. This includes:

- Loan term, interest rate, and loan amount

- Monthly mortgage payment estimates

- Closing costs include government fees, origination, and underwriting.

- The amount of money you will need to bring to closing. Also known as cash to close

- Loan disclosures

This document should be carefully reviewed before closing on a home. To ensure there are no discrepancies, you will want to compare the Closing Disclosure with the loan estimate.

For any errors you discover, please contact your lender. This may delay closing but it must be corrected before you sign the document.

Disclosure from the seller

The seller must complete a Seller’s Disclosure to list all known defects on the property. This document could have an impact on your decision to buy the house. These defects could include water damage, poor insulation, repair history, foundation issues, or infestations.

You should carefully read the disclosures as they may contain important issues that you didn’t notice on your last walkthrough. You have one last chance to find out more about the house before you make a big purchase. Houses are usually subject to a “no return policy”. Seller disclosures can save you thousands or even prevent buyer’s regret.

Ask the seller for more information or have a home inspector examine the details. To determine if the house is worth fixing or living in, you will need to gather as much information as possible.

Not all states require seller disclosures to be disclosed. Talk to a realty agent to find out what is required in your state.

You can negotiate with the seller to pay for repairs or to take the cost off of your purchase price if you are still interested in purchasing the home.

Title documents

A title company will conduct a title search on your behalf to verify that the seller is the owner of the property. This will allow you to legally sell the house. To prevent homeowners from being harassed by former owners for unpaid debts, the company will also search for liens on the property.

An escrow company or real estate attorney will examine the title documents to verify that the title is correct. The seller usually owns the title to the property. There will not be any liens or other issues with the title.

Request for a loan

Your lender will create a copy of the original application to close your loan application. It is important to check the original application for accuracy. If there are any changes, you should let your lender know. Any job changes or new debts should be reported to your lender, as they can impact the terms of your loan.

Preparing your finances for closing day

The Closing Disclosure should clearly state what you will need to pay on closing day. Here’s a quick overview of the expenses you may have to pay by your lender, seller, or yourself.

Closing costs

Your lender and any third parties involved in closing your loan will be charged closing costs. These fees are usually between 2% and 6% of the home’s purchase price and include a variety of fees such as the appraisal, origination, title, and application fees.

Depending on what type of loan you take and how much you pay, you may have to pay mortgage insurance.

Remember that closing costs may not be the same as prepaid expenses.

Earnest money

Earnest money is money that you deposit to show the seller that you are serious about purchasing their home. It also protects the seller in the event of your decision to withdraw from the deal.

The money is kept in an escrow account until the deal is complete. Once that happens, it can be applied to your down payment and closing costs.

Lender credits

In exchange for a higher interest rate, the lender may offer you lender credits to help with closing costs. This is a great option for buyers with limited cash to cover closing costs. A higher interest rate will mean that you’ll pay more interest over the term of the loan.

Cash to close

Cash to close refers to the sum of money (closing costs included) that you will need on closing day. The majority of cash you need to close is made up by your down payment. Your down payment can vary depending on the loan you have.

It could be as low as 3% or as high as you want. You may not need to make a down payment if you have a government-backed loan like a USDA loan or VA loan.

You may be eligible for credits or deductions if you have already paid certain payments to your lender, including your earnest money deposit.

Seller concessions

Sometimes, a seller will pay part of your closing costs. Remember to include any seller concessions if you have negotiated for the seller to pay a portion of your closing costs.

Dry closing

Dry closing is when all parties agree that the closing will proceed even though funds disbursement will take place after the closing. All other closing requirements for the loan can be met at this point.

The seller remains the owner of the property until they receive their funds. Buyers will not legally own the property until they have their mortgage funded.

Plan what to bring to the table

You will receive most of the closing documents that you’ll need to review and sign on closing. You will need to bring some items on closing day. Make sure to make a list so you can check off all your items while packing. These are the essential items to start your list:

- An identification form, such as a driver’s licence, passport, or government-issued photo ID

- A cashier’s or certified check in the amount due to closing costs or proof that a wire transfer has been completed (cash or personal checks are usually not accepted).

- Compare your Closing Disclosure with the final paperwork

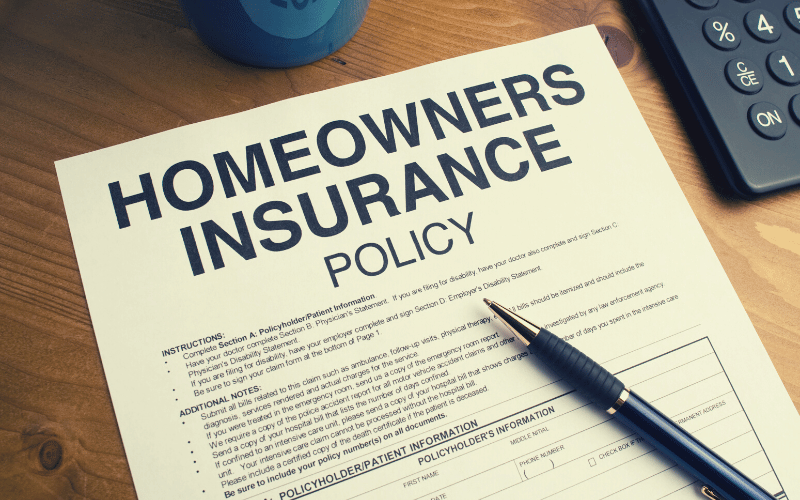

- You must provide proof of homeowner’s insurance

A list of contacts is also a good idea to have in case there are any problems. If they are not available at closing, this list could include your attorney or real estate agent.

Selecting a homeowners insurance policy

Lenders require that buyers obtain a homeowners insurance policy for their new home. They also need to show proof of insurance prior to or during closing.

Your home’s features and condition, as well as the amount of coverage you want and your willingness to pay for a deductible on homeowners insurance, will all affect the cost of your insurance.

How to avoid common roadblocks to closing

Some roadblocks may not be within your control. For example, a title search could reveal a lien against the house, a lower appraisal than anticipated, or a home inspection that uncovers an unknown problem with the property. There are some delays you can control that you can avoid.

Complete all lender requests as soon as possible

The buyer has control over the most common cause of delay: financial issues. These can occur when the buyer fails to submit required financial documents such as bank statements, tax returns, or pay stubs on time.

After your lender has started preparing for closing you can ask your loan officer for any additional information or documentation. You don’t need to wait for your lender to ask you for it. To avoid any disruptions, your lender may ask you for additional information or clarification.

Avoid financial changes that affect your life

Buyers who take on additional debt, get a new job, or miss a payment can have financial problems. These actions could affect your loan terms or even impact your eligibility for a mortgage.

When you are applying for mortgage preapproval be sure to keep your finances in order. Avoid big purchases, maxing your credit cards, opening new credit accounts, or missing your monthly payment.

Beware of mortgage scams

Before signing any documents or transferring funds, you should be aware of red flags. Phishing for mortgage wire fraud is a common scam. It uses fake email addresses, phone numbers, or websites to pretend to be your lender or real estate agent.

Hackers can convince home buyers to send their down payment or closing costs to a fake account by sending them emails that appear authentic.

This will prevent you from being in this situation. Always review your documents and do not respond to any last-minute requests or “act quickly” requests.

The bottom line: It is possible to simplify the process by learning about real estate closings beforehand

The home-buying process doesn’t need to be complicated or confusing. It is worth taking the time to learn about the whole process from beginning to end. This will allow you to better navigate the difficulties of buying a home and closing on your mortgage.

It can help you avoid delays and make closing days more enjoyable by knowing what documents and information to send to your lender.

{kind=link}